Double 7’s Strategy

This simple double 7’s strategy was revealed in the book Short Term Strategies that Work: A Quantified Guide to Trading Stocks and ETFs, by Larry Connors and Cesar Alvarez. It’s a mean reversion strategy looking to buy dips and sell on strength and was initially designed for ETFs. In testing it has shown an extremely high winning percentage of trades. The basic rules are:

- The stock must be above its 200 day moving average.

- If the stock closes at a 7-day low, then buy.

- Sell the position if it closes at a 7-day high.

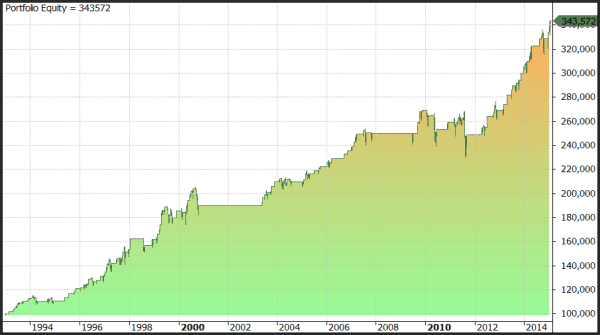

The following chart shows the strategy equity growth on the S&P 500 ETF since 1993 with a 77% win rate and very minimal volatility.

However, whilst the above appears favourable, the annual return is just 7%. The reason is simple; trading only one instrument, in this case the S&P 500 ETF, means just 119 trades in about 22 years. In order to increase profitability we’ll need to also increase trade frequency and to do that we need to trade a basket of ETFs or a basket of stocks.

Let’s now test it on a basket of Australian stocks, namely the ASX-100. We’ll allocate 10% of equity to 10 positions and we’ll use historical constituents to remove survivorship bias. This shows an annual return of 15.65% with a winning rate of trades just over 70%. Not too bad for such a simple set of rules.

![]()