One Trade, Two Worlds

The defining market story of 2026 thus far has been the AI trade, as it was in 2025 and 2024. But this year it has done something new. It broadened. The AI rally, initially driven by a small minority of mega-cap stocks, has widened into a full-blown corporate hardware arms race. But this process has not been distributed globally, and the rush has sorted the world’s equity markets into two camps: those with exposure to it and those without.

Australia has landed firmly in the second camp. If you had solely focused on the ASX this year, you might have mistakenly assumed it was uneventful. Across 2026, the ASX 200 index has clearly remained rangebound, oscillating around breakeven without much conviction.

But that flat line disguises a much bigger problem. Beneath it sits one of the weakest year-to-date performances in the developed world. To understand the more profound problem, though, we must first zoom out, not in.

The Dividing Line

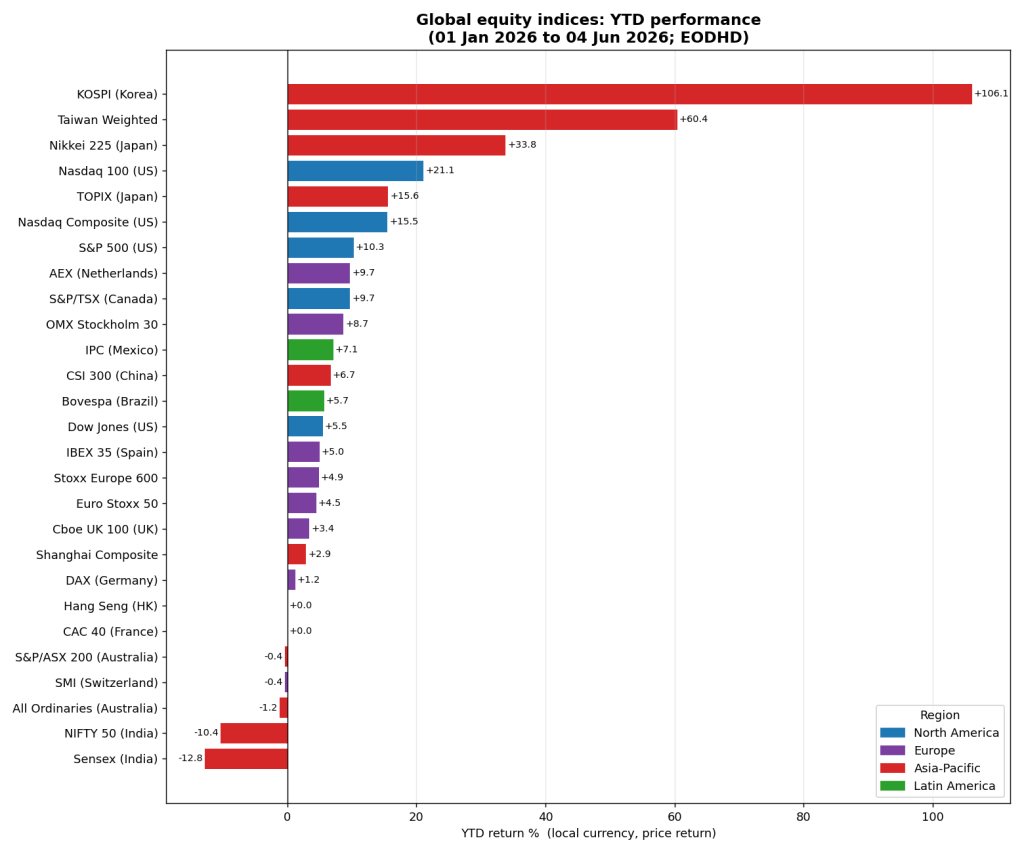

If we line up 27 of the world’s major equity indices and rank them by performance, a clear pattern emerges. At the are top indexes from Korea, Taiwan, Japan, and the United States. No deep analysis is required to find what puts them there, it’s almost embarrassingly simple: exposure to AI and semiconductors. The indices at the top are stuffed with chipmakers, memory producers, and all the hardware that AI requires to run.

So where does Australia fit into all of this? Bluntly put: it doesn’t. The ASX indices appear right down the bottom of the list, alongside Switzerland and trailing every European index.

Australia has no semi-conductor industry and no meaningful AI exposure to speak of. The tech industry in Australia primarily focuses on software and services, which have been declining globally amidst AI disruption. The two largest ASX tech companies, WiseTech and Xero, are down -26% and -40% YTD. Only a handful of smaller tech stocks like NextDC and Megaport have caught the AI tailwind.

We can see this same phenomenon play out in the UK, which has a similarly software-focused tech industry. The UK’s tech sector has fallen -10% YTD, almost identical to the ASX tech sector.

So, this isn’t really an Australian story so much as a global one, but Australia just happens to be one of the cleanest examples of what missing out looks like.

The AI Trade Matured

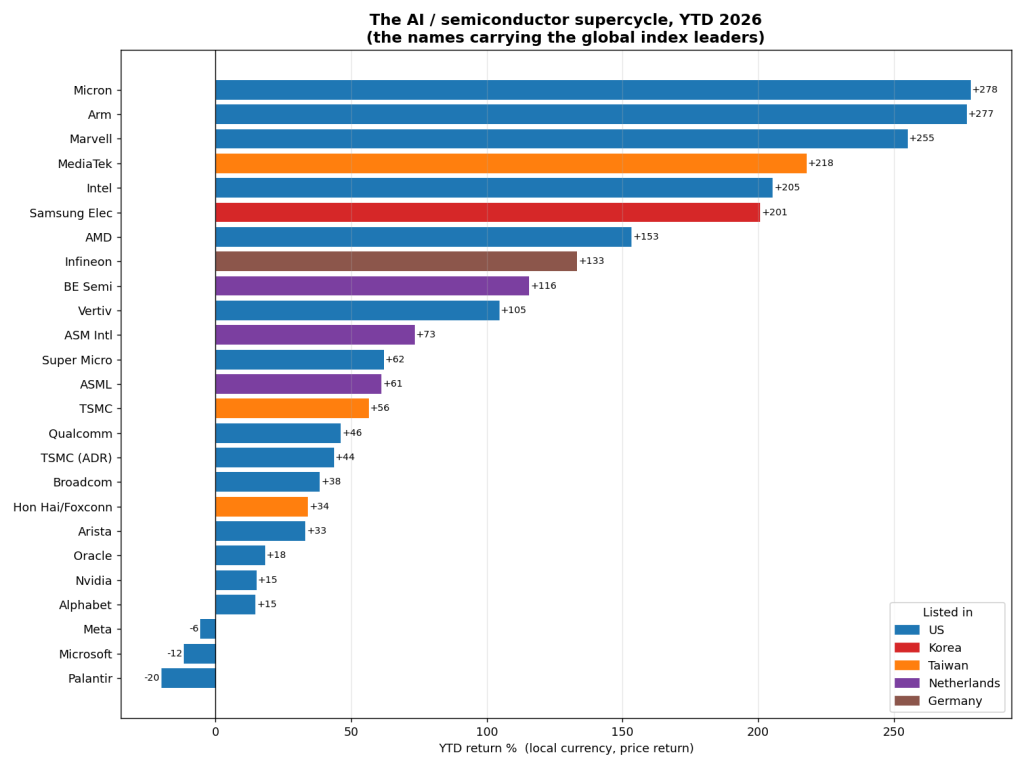

Over the past few years, the AI rally has been dangerously narrow, dominated by a small cadre of leaders, namely the “Magnificent Seven“. Nvidia, of course, led the charge from far in front, while other chipmakers lagged behind, largely dragged along in sympathy.

Across the last 12 months, however, we’ve seen that dominance falter. The rally has broadened, but not to other chipmakers or AI developers, nor to the wider market as a whole; specifically, it has moved across into hardware. The current move is overwhelmingly an AI hardware push.

The numbers tell the story. The original AI poster children have slipped down the leaderboard. Nvidia is up a relatively modest 15%, while Microsoft has actually fallen. At the top end of the chart, the memory and hardware names have gone vertical: Micron, MediaTek, and Samsung are up 200% YTD (in their local currencies). The centre of gravity has moved from a narrow band of chip designers to a much wider set of hardware manufacturers, specifically, the companies that dominate the markets at the top of the indices table.

What “left behind” looks like underneath

Missing out on the AI hardware trade isn’t simply a matter of being left stagnant. Headline index returns paint a deceptive picture of a flat ASX 200, but look beneath the surface, and the picture changes materially. The simplest way to see this situation is to ask, how is the average stock actually doing?

Indices like the ASX 200 are weighted by market capitalisation, so the biggest companies skew the headline number significantly. An equal-weighted version, by contrast, gives the smallest company the same sway as the largest. The equal-weighted index presents a significantly different narrative. Where the cap-weighted ASX 200 is roughly flat, its equal-weighted version is down -5%. Broaden this out to the All Ordinaries, and the typical stock is closer to -6%.

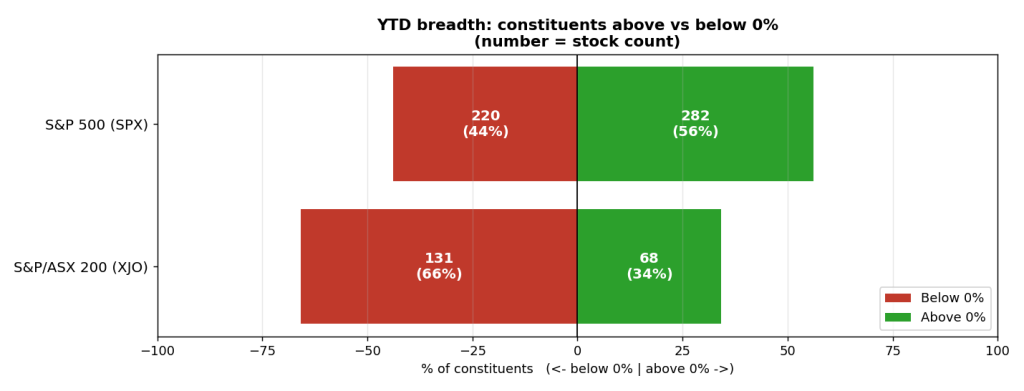

This is a problem of breadth, that is, how many stocks are actually participating in a market move. The bluntest demonstration of this is simply to count the number of winners and losers without considering returns at all:

- S&P 500: ~56% of stocks positive

- Russell 1000: ~53% positive.

- ASX 200: ~34% positive

- All Ordinaries: ~33% positive

Roughly two of every three stocks on the ASX 200 are negative YTD, compared to less than one in two for the US. This is true for both larger and smaller caps. The picture of a “flat” ASX is clearly deceiving.

The effect on traders is stark. Trend-following strategies, which depend on smaller breakout stocks, struggle to gain traction, while top-end strategies struggle to achieve significant growth without heavily investing in a select few market leaders.

Some wounds are home grown

AI is not solely responsible for Australia’s weakness. Some of it is squarely local.

The standout is the healthcare sector, which is down 33% YTD against declines of just 4–5% in the US and UK. A large share of that is a single stock: CSL, which makes up around a quarter of the ASX health sector and has fallen close to 47%, accounting for roughly half the sector’s entire decline on its own. But it isn’t only CSL; Cochlear is down 64%, ResMed 28% and Pro Medicus 28%.

The common thread is a stronger Australian dollar eating into offshore earnings and a higher-for-longer rate environment dampening growth stocks. These are domestic headwinds layered on top of the global one.

What’s keeping the ASX afloat?

What stocks are keeping the ASX from falling if only a few names are propping it up? The answer will be a familiar one to Australian investors: resources.

Energy and materials have been the only consistent green corners of the market, riding a global commodity bid. And because the big miners carry such enormous index weighting, they’ve been able to single-handedly hold up the index headline numbers.

This global commodity bid, though, is not a global commodity boom. Current commodity drivers are mostly from geopolitical supply disruptions (the US-Iran war), energy transition, and precious metals. Comparatively, the 2000s commodity boom was driven largely by rapid industrialisation in developing countries, which required huge amounts of raw materials that Australia happily provided.

The AI hardware boom, meanwhile, has not triggered a similar broad commodity rush for a simple reason: AI hardware is value-dense but material-light. A cutting-edge computer chip is an incredibly sophisticated piece of technology that requires a relatively tiny amount of physical matter. So, a trillion-dollar investment in AI hardware consumes far fewer raw commodities than the same investment in construction. The AI industry does not have no effect on commodities, but the raw tonnage is entirely different.

Is the ASX dead then?

All of this amounts to a discouraging picture for the Australian investor, but the encouraging part of all this is that almost none of it is permanent. Australia hasn’t been left behind because something is structurally broken; it’s been left behind because the investment theme driving global markets right now happens to be one it has almost no exposure to. But trades rotate and commodity cycles turn. The strong dollar and high rates pressuring healthcare today won’t last forever. The ASX is having a poor year for an unusually specific and identifiable reason, but that’s a very different thing from a market in decline.

To receive weekly market insights and trading tips delivered straight to your inbox. Sign up for our newsletter here. Or else why not look at our membership portfolios? These can be accessed while on our 14 day free trial.