Leveraged ETFs Explained and When to Use Them

A question that has arisen a few times from clients is, “Can I substitute an index ETF in the All Weather with a leveraged version of the same?” While on the surface, this seems like a reasonable idea (why not multiply the returns?), it points to a misunderstanding of how leveraged ETFs function and shows how traders can easily fall into the volatility drag trap. Let’s take a look at how leveraged ETFs work, when we should avoid them, and when the best time to invest in them is.

What are leveraged ETFs?

Leveraged ETFs are essentially what they say on the tin. Leveraged ETFs are exchange-traded funds that utilize leverage to enhance both returns and losses. Managers of leveraged ETFs use derivatives such as futures contracts to trade outsized positions in the underlying assets, thereby providing an ETF that tracks a multiple of that underlying asset. I.e., a 3x leveraged Nasdaq-100 ETF will see three times the loss or gain of the Nasdaq-100.

Leveraged ETFs offer an enticing deal: easy access to amplified returns (most suggest 2x or 3x) without the need for options, futures, or the burden of setting up a margin account. For example, my SelfWealth account, which has no mechanism for margin at all, is able to purchase a number of leveraged ETFs with no additional approval required. Typically, access to margin requires many forms and means testing to prove you are suitably experienced to trade with margin.

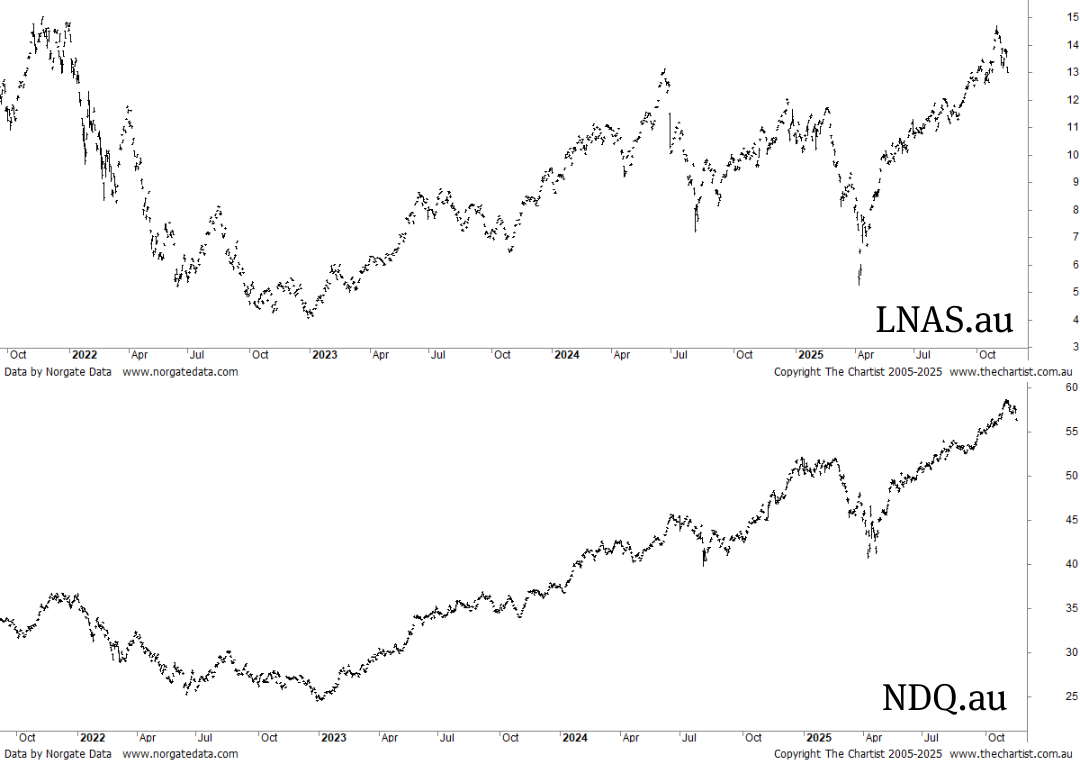

One example of a leveraged ETF I can purchase on the ASX is the Global X Ultra Long Nasdaq 100 Complex ETF (LNAS.au), which tracks the Nasdaq 100 and provides returns ranging from 2x to 2.75x of the Nasdaq 100’s movements. However, a look at the historical performance for LNAS shows a stock with a returns completely different to a comparable unleveraged ETF, NDQ.au, which tracks the straight Nasdaq 100.

You would probably expect these charts to look relatively similar, just with different scales, but as we can see, the charts look like two entirely unrelated assets. While the Nasdaq fell and then quickly recovered to 2021 heights, LNAS still has not fully recovered those losses. So, what’s going on?

How Leveraged ETFs Work

A common misconception is that a leveraged ETF will simply multiply an asset’s returns for a given time period. E.g., if the Nasdaq 100 gained 10% in a year, a 3x leveraged version would gain 30%. But this is not the case.

Leveraged ETFs are typically designed to deliver a multiple of an index’s daily return, not its long-term performance. Each day the fund manager needs to reset the ETF’s exposure back to the target rate (i.e., 3x). This resetting means that the gains and losses of the ETF compound in a non-linear way over time.

If the index ETF gains 1% in a day, then a 3x leveraged version will gain 3% for that same day. Conversely, if the index ETF loses 1% in a day, the leveraged ETF loses 3%. The problem that therefore arises is that the distance required to get back to breakeven can compound drastically, even if significant losses are not occurring on the underlying index.

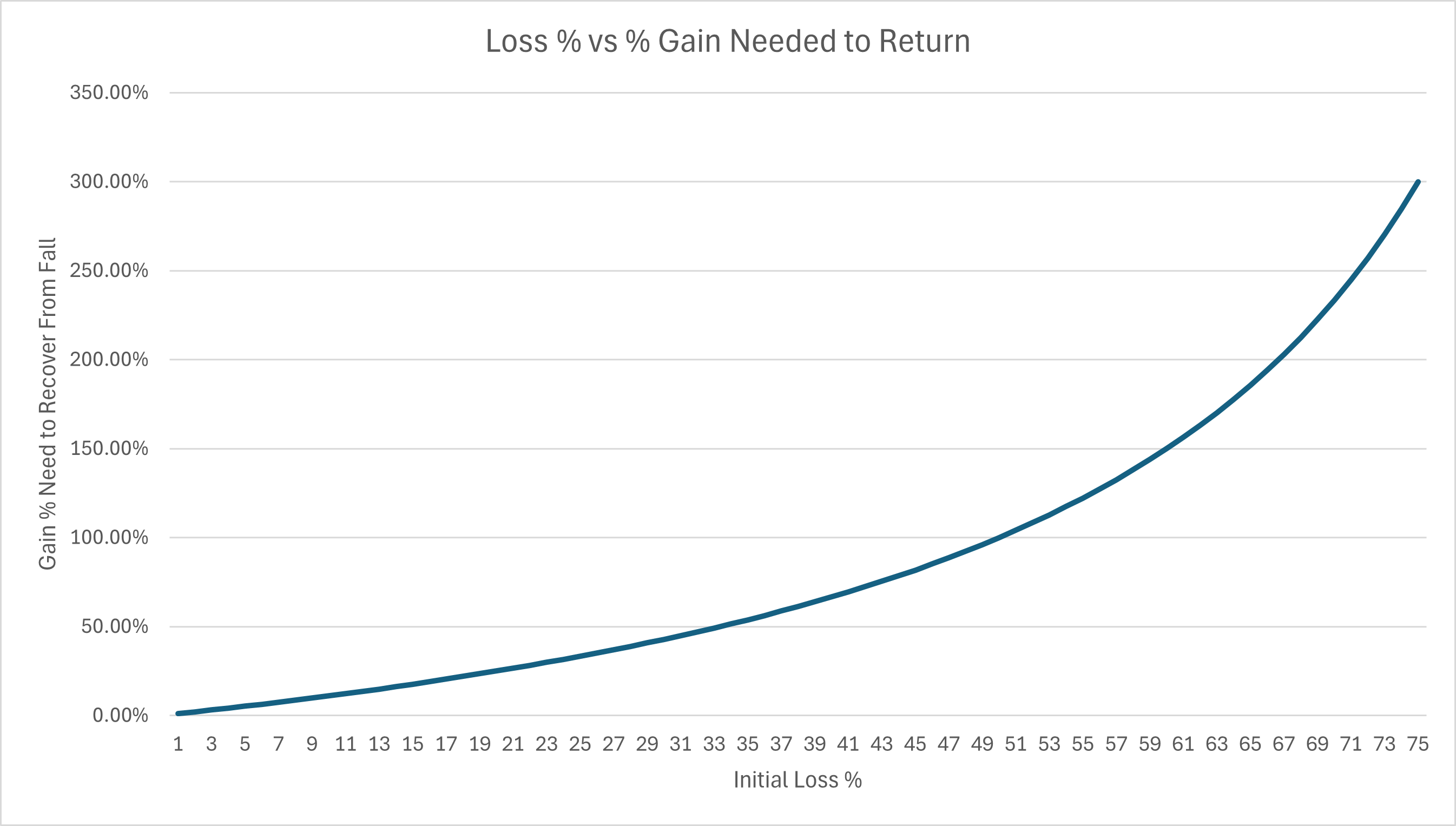

After any loss on an investment, a percentage gain greater than the percentage loss is needed to recover back to its original value; this is true of both leveraged and unleveraged positions. For example, a loss of 10% in one day requires a gain of 11.11% the next day to arrive back at its original position. But a 30% loss attained on the same day by the 3x leveraged ETF requires a 42.86% gain to return to breakeven. You can see that the difference in the gain required has grown. These additional losses can add up quickly over time, especially as the base value for the margin is lowered with each day. So, even if the underlying index or asset is flat over time, the leveraged equivalent can decline due to these small losses adding up. This is known as volatility drag.

The asymmetry in losses taken versus the value needed to return grows rapidly as the loss increases. The problem becomes especially apparent in volatile or choppy markets, and particularly sideways-moving markets. As repeated losses occur, the little differences in the distance to return add up. And because the leverage starting balance is reset every day, the problem compounds over time. Therefore, once a fund has suffered significant falls, they’re not just deeper but also stickier. This volatility drag is an inherent element in any leveraged fund or ETF.

So, what is the point of leveraged ETFs then?

As we’ve seen, across the long term, leveraged ETFs suffer from significant volatility drag; this is unavoidable. But if that made leveraged ETFs a “bad” investment then they simply would not exist. The existence of this volatility drag is not so much a flaw as it is a mathematical reality. Fund managers are not naive to the existence of volatility drag or even trying to avoid it. Leveraged ETFs can still be traded profitably by those who understand the problem and know how to navigate it. Leveraged ETFs do not exist for buy and hold investment strategies in the way a standard index ETF does, but rather for well-timed, short-term trading which navigates the pitfalls.

Leveraged ETFs are ideal for trading:

- In low volatility uptrends, where positive days occur more frequently than negative.

- Across short-term time periods (holding intra-day or for less than a week).

- Environments where there is a clear upward momentum.

You should avoid leveraged ETFs when:

- The market is moving sideways.

- Volatility is high, especially when the direction is unclear.

- Times of strong reversals (i.e., earnings periods).

Leveraged ETFs can be a useful tool in a trading arsenal, but they are inherently hyper-responsive to market movements, which can create big issues if held long term. Knowing how they function and when suitable conditions for trading them exist is of utmost importance for success.

To read more about diversifying with ETFs take a look at another article here.